S&P500 Series Pt. 2: History and Relevance of the Index

Introduction

Continuing our series on the S&P500 Index, this instalment will look at the bigger picture. Investors primarily use one of two main methods of analysis, technical and fundamental. Whereas technical analysis concerns itself with market trading trends, and by extension traders psychology, fundamental analysis concerns itself with the substantive value of the asset traded. Understanding the background and context of the S&P500 will aid in the fundamental analysis aspect of trading this index, beyond simple pattern recognition.

History

S&P stands for Standard and Poors, named after the Standard & Poor's Financial Services LLC. Henry Varnum Poor, the companies founder first began tracking a small number of stocks as an index back in 1923, called the Composite Index. In 1941 the original company (Poor's Publishing) merged with Standard Statistics, and by 1957 the Composite Index had expanded to 500 stocks and was renamed the S&P500. Currently, regardless of name, the index includes 505 American companies and is almost unanimously considered to be the best indicator of the US economy.

Selection Criteria

Evident by the name the Index tracks 505 large US companies which have common stock listed not the NYSE, NASDAQ, or the Cboe BZX Exchange. The companies included range from Industrial Conglomerates such as 3M Company, to tech-giants such as Oracle, and Asset Management firms such as BlackRock. The included companies are selected by a committee that considers eligibility based around eight primary criteria: market capitalization, liquidity, domicile, public float, sector classification, financial viability, and length of time publicly traded and stock exchange. Specific examples regarding these criteria include: a market cap of $6.1 billion, minimum monthly trading volume of 250,000 shares, 50% of outstanding shares are floating, and positive as-reported earnings for the most recent five quarters.

General Price History

On January 3, 1950, the closing level was a mere $16.66. By June 4, 1968, the closing price first broke $100 at a closing rate of $100.38. February 2, 1998 saw the Index reach $1,001.27, and August 26, 2014 $2,000.02. As of the writing of this article the Index is traded at $2,822.48. The index is updated every 15 seconds during trading hours, and published by Reuters America. Due to the fact that the Index represents the weighted relative average of 505 large, established and profitable companies, fluctuations in the Index are effected by large scale factors primarily. For this reason it’s often utilised as a political talking points in reference to Economic health. The Trump administration particularly has been fond of siting high index levels as evidence for good political performance. “S&P 500 HITS ALL-TIME HIGH Congratulations USA!”-Donald Trump’s private Twitter on 20 Sep 2018. As many political talking points are, its important to recognise that the performance of the S&P is never solely due to the actions of any particular administration.

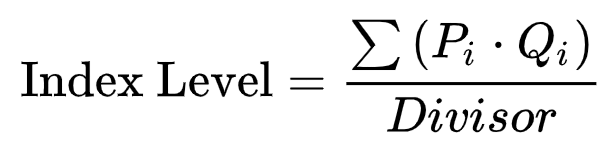

Maintenance and Calculation

The way by which the final Index level is determined is with a simple formula. Its the sum of the market capitalisation (shares outstanding multiplied by the share price), divided by a divisor. As an example, if the total adjusted market capitalisation of the 505 component stocks is US$13 trillion and the divisor is set at 8.933 billion, then the S&P 500 Index value would be 1,455.28. This divisor is not constant and serves the specific task of factoring for company action that changes the share price without any fundamental changes in value. The divisor is adjusted in the case of stock issuance, spin-offs, mergers, or similar structural changes, as to avoid alterations in the Index price, keeping it more reliable as a benchmark.

Advantages and Disadvantages of the S&P500 as a Benchmark

It is common knowledge that the S&P500 performance is used by investors and asset managers globally as a benchmark for performance. Beating the return on investment that is annually generated by the index is often considered to be an indicator of a successful and uniquely profitable investment strategy. The returns generated by the Index back when it only included 90 stocks in 1926, until now has been an annual 10%. It should be noted that more attention should be given to this figure than simply assuming a doubling of ones money every 10 years. Accurate calculations of average returns, after considering the entirety of significant factors can be extremely difficult.

The central advantage of the Index as a benchmark is the wide market breadth included in the price. This generally indicates a broad view of the American Economy as a whole. On a practical level, an investor can compare their high or low returns to the macro environment. Lower returns that exceed the S&P500 during periods of low economic performance are not as bad as low returns during periods of high economic performance. A certain fraction of asset management returns are always subject to exogenous factors. These factors are shared in the performance of the S&P500 as well, thus it makes it easier to assess good or bad performance on indigenous factors of the investor himself.

Additionally the companies included in the Index are updated on a quarterly basis, through criteria previously discussed. This prevents uniquely poor performance of a single company (for example market capitalisation dropping below the benchmark), to disproportionally reflect on the Index value, and therefor give an inaccurate representation of market conditions.

There exist several drawbacks however concerning the usage of the index as a benchmark. Firstly, many investor portfolios are diversified beyond stocks, and can include commodities such as precious metal, bonds, CDO’s (collateralized debt obligation), and a multitude of other financial vehicles. Since the S&P500 includes nothing such as these, it can be deceptive to measure a diversified portfolio against stock performance exclusively.

Furthermore, the content of the S&P500 is by definition limited to very large companies. This fails to then accurately capture an investors ability to for example ,recognise tremendous growth potential within smaller companies, who's price performance can be drastically different from established firms.

Finally, as a result of its nature the index suffers from an implicit problem. Due to the constant updating of the index companies significantly poor performance does not reflect on the index price, yet disproportionately good performance can. The biggest 50 firms account for over half of the market capitalisation of the S&P500 total $23.7 trillion. As a result, a change in the market capitalisation can significantly affect the index price. An investors performance can then be perceived as relatively good or bad when in reality it may only be one company that has dragged the index price up or down, and therefor does not reflect the economy as a whole.

Editing by Tom Handels